What Every SoCal Condo Buyer Needs to Know Right Now?

You found the perfect Southern California townhouse, your offer was accepted, and the numbers fit your budget perfectly. Then, deep in escrow, you get hit with a financial curveball.

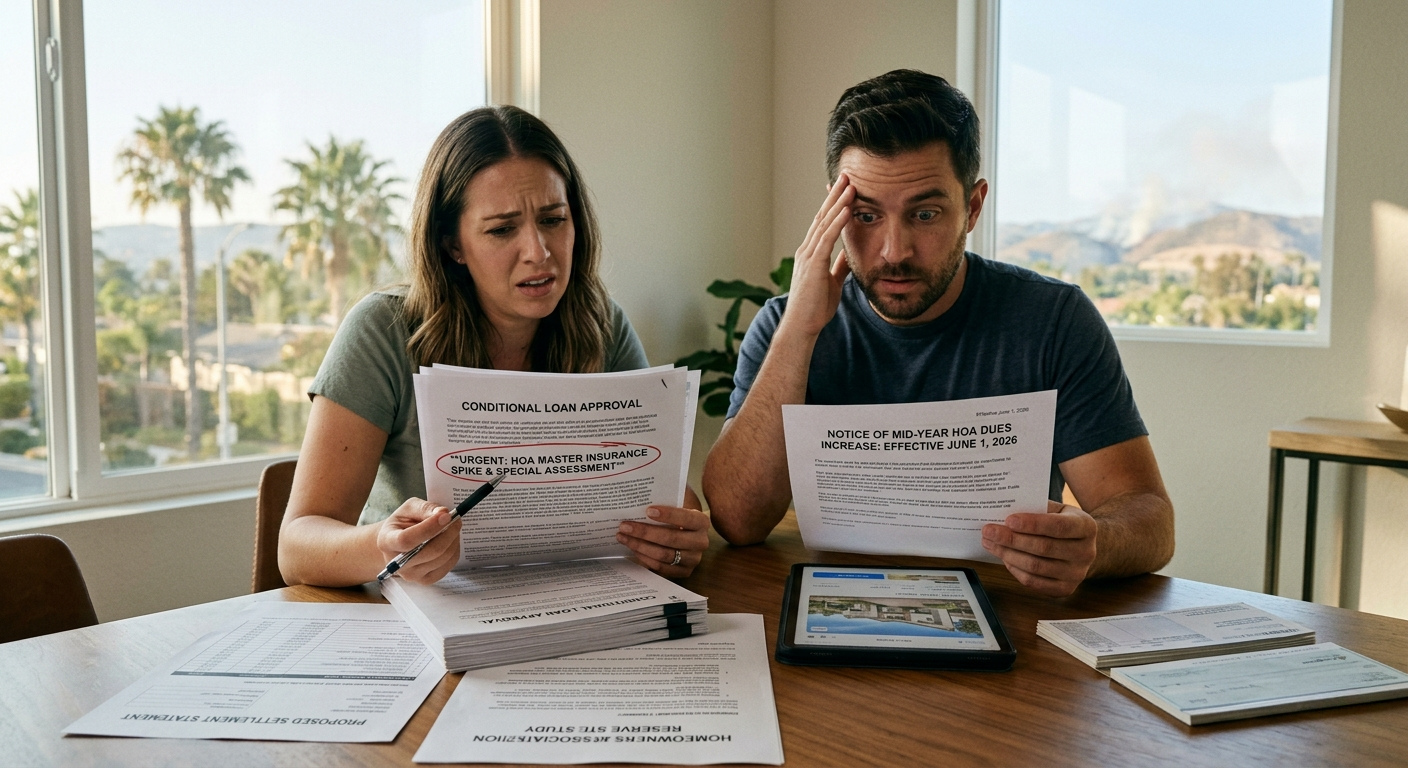

Right now, there is a massive sleeper topic catching buyers off guard: California’s property insurance crisis is quietly rocking Homeowners Associations (HOAs) and condo communities.

Here is what’s happening behind the scenes and how to protect your wallet.

Why HOA Fees Are Spiking?

We all know wildfire and climate risks have caused home insurance premiums to skyrocket for single-family homes. But HOAs have to buy insurance, too.

An HOA board must purchase a "master policy" to cover the community's physical structures. When these massive commercial policies renew, premiums are frequently doubling or tripling. To cover these sudden mid-year budget gaps, boards are forced to act fast, resulting in:

Steep Monthly Dues Hikes: Permanent increases to your monthly HOA fee.

Special Assessments: Surprise, one-time bills levied on every homeowner to cover an immediate shortfall, often costing thousands of dollars.

The Due Diligence Checklist

You don’t need to avoid condos; you just need to look under the hood before you lift your contingencies. Treat the HOA documents like a physical home inspection:

Review the Reserve Study: Check the HOA’s financial health. If their reserves are underfunded, they have no cushion to absorb an insurance spike, making a surprise assessment highly likely.

Read the Recent Meeting Minutes: Look back 6 to 12 months. Search for keywords like insurance renewal, premium increase, or budget shortfall. This is where the real financial truth hides.

Ask Point-Blank: Have your agent ask the seller's agent in writing if the board has discussed any upcoming dues increases or special assessments.

Turn a Tough Market Into a Win

Navigating today's market requires a game plan, but it also gives you leverage. The classic philosophy of "marry the house, date the rate" is still a winning move, especially when you pair it with a seller-funded rate buydown.

By negotiating a temporary rate buydown funded by the seller, you can significantly lower your mortgage payment for the first one to two years. This gives you a massive financial cushion to safely absorb any localized HOA shifts while you wait for interest rates to ease.

Protect your investment by doing your homework before you fully commit.

👉 Are you house hunting in SoCal or getting ready to open escrow?

Let's connect to make sure your budget is fully protected from hidden costs.